U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10

GENERAL FORM FOR REGISTRATION OF SECURITIES

Pursuant to Section 12(b) or (g) of The Securities Exchange Act of 1934

IANTHUS CAPITAL HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| British Columbia, Canada | 98-1360810 | |

| (State or other jurisdiction of | (I.R.S. employer | |

| incorporation or formation) | identification number) | |

| 420 Lexington Avenue, Suite 414, New York, NY | 10170 | |

| (Address of principal executive offices) | (Zip Code) |

(646) 518-9411

(Issuer’s Telephone Number)

Securities to be registered under Section 12(b) of the Act: None.

Securities to be registered under Section 12(g) of the Act: Common Shares, no par value

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filter | ☐ | Accelerated filter | ☐ | |

| Non-accelerated filter | ☒ | Smaller reporting company | ☒ | |

| Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided by Section 7(a)(2)(B) of the Securities Act. ☐

THE COMPANY

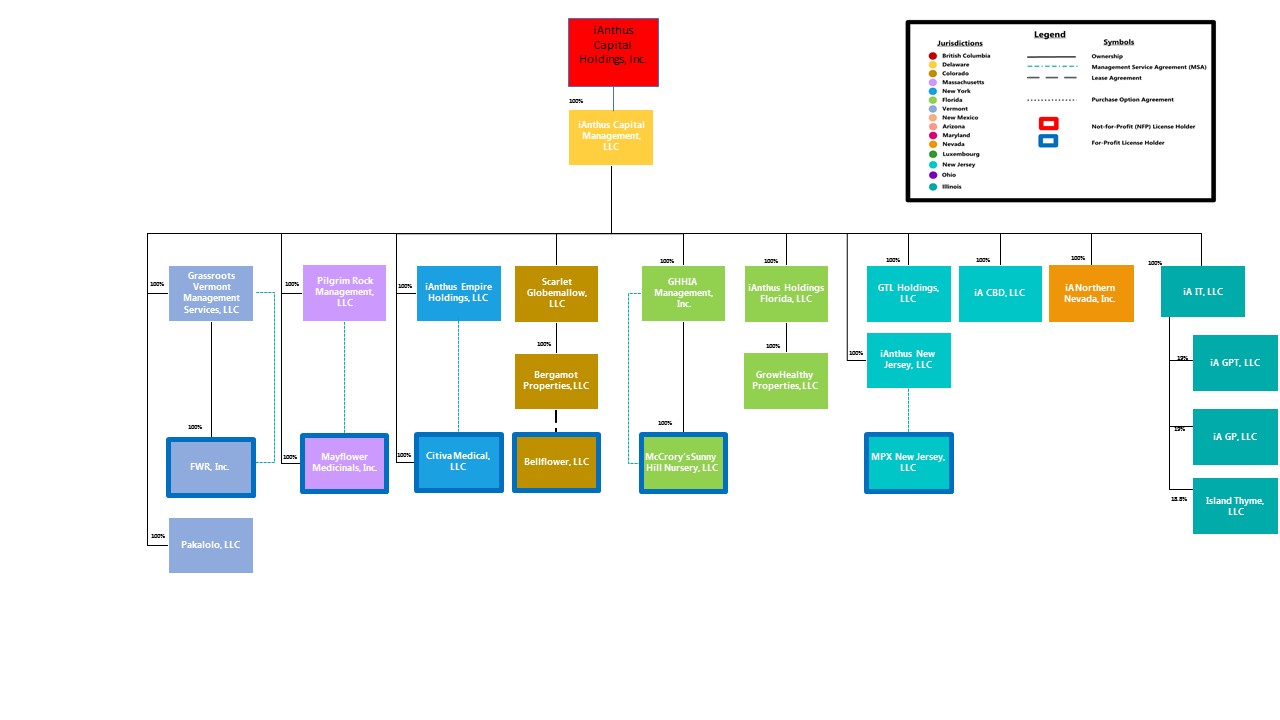

iAnthus Capital Holdings, Inc. (the “Company”) is a holding company with the subsidiaries set forth in the chart below.

ITEM 1. BUSINESS.

Unless the context indicates or suggests otherwise, references to “we,” “our,” “us,” the “Company,” or “iAnthus” refer to iAnthus Capital Holdings, Inc., a corporation organized under the laws of British Columbia, Canada, individually, or as the context requires, collectively with its subsidiaries.

Overview

We are a leading, vertically-integrated, multi-state owner and operator of licensed cannabis cultivation, processing and dispensary facilities and a developer, producer and distributor of innovative branded cannabis and cannabidiol (“CBD”) products in the United States. We are committed to creating a national retail brand and portfolio of branded cannabis and CBD products recognized in the United States.

Through our subsidiaries, we currently own and/or operate 29 dispensaries and 10 cultivation and/or processing facilities in nine U.S. states. In addition, we distribute cannabis and CBD products to over 200 dispensaries and CBD products to over 2,300 retail locations throughout the United States. Pursuant to our existing licenses, interests and contractual arrangements, we have the capacity to own and/or operate up to an additional 13 dispensaries in five states, plus an uncapped number of dispensaries in Florida and up to 12 cultivation and/or processing facilities and we have the right to manufacture and distribute cannabis products in nine U.S. states.

Our multi-state operations encompass the full spectrum of medical and adult-use cannabis and CBD enterprises, including cultivation, processing, product development, wholesale-distribution and retail. Cannabis products offered by us include flower and trim, products containing cannabis flower and trim (such as pre-rolls), cannabis infused products (such as topical creams and edibles) and products containing cannabis extracts (such as vape cartridges, concentrates, live resins, wax products, oils and tinctures). Our CBD products include products designed for wellness (such as topical creams, tinctures and sprays) and products designed for beauty and skincare (such as lotions, creams, haircare products, lip balms and bath bombs).

Operations

Cultivation. We cultivate multiple strains of cannabis plants within our licensed cultivation facilities across the United States. We believe that our facilities are designed, managed and operated to cultivate high-quality products in a cost-effective manner. Our cultivation process uses all parts of the cannabis plant, including flower and trim (“biomass”), to produce cannabis products that we sell at our dispensaries and distribute to third parties on a wholesale basis. We have 12 cultivation and processing licenses in nine U.S. states, with approximately 417,000 square feet of cultivation and processing space which is fully built-out, approximately 400,000 square feet of space which is under construction and the ability to expand to a total of approximately 817,000 square feet of space within our existing lots. We currently have the ability to harvest approximately 56,000 pounds of biomass annually in our existing cultivation space, and we believe that we will have the ability to harvest approximately 195,000 pounds of biomass annually if we are able to use all of our projected cultivation space, including the cultivation space that is currently under construction and the additional unused cultivation space within our existing lots.

Product Development and Processing. We develop and sell cannabis products for medical and adult-use and CBD products for wellness, beauty and skincare. Biomass is processed into oil and resin that is used to develop numerous cannabis-extracted products, including vape pen oils, lotions, tinctures, other concentrates and edibles. We typically conduct product development and processing activities within our cultivation facilities and CBD products are manufactured in third-party manufacturing facilities. Processing procedures include developing formulations and packaging for all cannabis branded products, including the brands we own (such as Mayflower Medicinals, Black Label and Melting Point Extracts (MPX)), as well as brands that we manufacture and sell pursuant to our white label and/or licensing agreements.

Distribution.

Wholesale.

We distribute our cannabis products through our wholesale channel to over 200 dispensaries, including our own dispensaries. Our MPX and Black Label branded products are distributed in over 170 dispensaries in Arizona, Maryland and Nevada. Our CBD products, which are produced under the brand name CBD For Life, are distributed through a mass market retail model, including online at www.cbdforlife.us and in over 2,300 retail locations across the United States. Wholesale customers for our CBD products include dispensaries, local retailers and several national retailers. We also have distribution and sales partnerships for our CBD products.

Retail.

We currently own and/or operate 29 dispensaries for the sale of medical and/or adult-use cannabis, CBD and ancillary products. These dispensaries sell products that have been cultivated, developed and processed by us as well as third parties, in states where such sales are permitted. We own and/or operate licensed dispensaries in prime markets, including Baltimore, Bethesda, Boston, Brooklyn, Miami, Orlando, Phoenix, Staten Island and West Palm Beach, and we plan to open additional locations in other prime markets such as Atlantic City and Las Vegas.

-1-

Our Marijuana Dispensaries, Cultivation and Manufacturing

The table below provides a summary of our licensed operations:

| State | Licensed Entity | Type of Investment | Permitted Number of Facilities | |||

| Arizona | ABACA, Inc. (“ABACA”) The Healing Center Wellness Center, LLC (“THCWC”) Health for Life, Inc. (“HFL”) Soothing Options, Inc. (“Soothing Options”) |

See Note 1 | 4 dispensaries2 8 cultivation2 8 processing2 | |||

| Colorado | See Note 3 | See Note 3 | See Note 3 | |||

| Florida | McCrory’s Sunny Hill Nursery, LLC (“McCrory’s”) | Ownership (100%)4 | No dispensary cap5 1 cultivation6 1 processing6 | |||

| Maryland | LMS Wellness, Benefit LLC (“LMS”) GreenMart of Maryland, LLC (“GMMD”) Rosebud Organics, Inc. (“Rosebud”) Budding Rose, Inc. (“Budding Rose”) |

See Note 7 | 3 dispensaries 1 processing | |||

| Massachusetts | Mayflower Medicinals, Inc. (“Mayflower”) Cannatech Medicinals, Inc. (“Cannatech”) |

Ownership (100%)8 | 3 medical dispensaries9 3 adult-use dispensaries9 3 medical cultivation/processing10 3 adult-use cultivation10 3 adult-use processing10 | |||

| Nevada | GreenMart of Nevada NLV, LLC (“GMNV”) | See Note 11 | 3 dispensaries11 1 cultivation12 1 processing12 | |||

| New Jersey | MPX New Jersey, LLC (“MPX NJ”) | See Note 13 | 3 dispensaries14 1 cultivation15 1 processing15 | |||

| New York | Citiva Medical, LLC (“Citiva”) | Ownership (100%) | 4 dispensaries16 1 cultivation16 1 processing16 | |||

| Vermont | FWR Inc. d/b/a Grassroots Vermont (“GRVT”) | Ownership (100%)17 | 2 dispensaries18 1 cultivation18 1 processing18 | |||

| United States | iA CBD, LLC (“iA CBD”) | Ownership (100%) | See Note 19 |

| (1) | ABACA, HFL, Soothing Options and THCWC are non-profit entities. Our wholly owned subsidiary, iAnthus Arizona, LLC (“iA AZ”), has entered into management agreements with ABACA, HFL, Soothing Options and THCWC, each of which holds an Arizona Medical Marijuana Dispensary Registration Certificate. |

| (2) | An Arizona Medical Marijuana Dispensary Registration Certificate permits its holder to operate one medical cannabis dispensary which can be co-located with one medical cannabis cultivation and processing facility and one separately located cultivation and processing facility. Through ABACA, HFL, Soothing Options and THCWC, we currently operate four medical cannabis dispensaries and three facilities for medical cannabis cultivation and processing, two of which are co-located with their affiliated dispensaries. The Dispensary Registration Certificates held by ABACA, HFL, Soothing Options and THCWC, collectively allow for the operation of up to four medical cannabis dispensaries and up to eight medical cannabis cultivation and processing facilities, subject to regulatory approval. |

-2-

| (3) | We do not currently have a license to operate a cannabis business in Colorado; however, on December 5, 2016, in related transactions, we, through our wholly-owned subsidiaries, Scarlet Globemallow, LLC (“Scarlet”) and Bergamot Properties, LLC (“Bergamot”) acquired certain non-cannabis assets of Organix, LLC (“Organix”) and the real estate holdings of Organix’s affiliate, DB Land Holdings, Inc., consisting of a 12,000 square foot cultivation facility in Denver, Colorado. Bergamot also purchased a dispensary located in Breckenridge, Colorado from a third-party. |

| (4) | We own 100% of GHHIA Management, Inc. (“GHHIA”), which holds an exclusive 40-year management agreement to operate the medical cannabis business associated with the Florida Medical Marijuana Treatment Center (“MMTC”) license issued to McCrory’s and held an option to acquire 100% of McCrory’s for a nominal consideration, subject to the approval of the Florida Department of Health. On August 14, 2019, the Florida Department of Health approved GHHIA’s option to acquire McCrory’s and GHHIA subsequently exercised the option. Accordingly, we, through our wholly-owned subsidiary GHHIA, now own 100% of McCrory’s. |

| (5) | Until April 1, 2020, Florida imposed a progressive limit on the number of medical cannabis dispensaries that could be operated by each vertically licensed MMTC based on the number of registered qualified medical cannabis patients in the state. This statutory cap, which permitted 25 dispensaries per MMTC, increasing by 5 dispensaries for each additional 100,000 patients registered in Florida’s Medical Marijuana Use Registry, expired on April 1, 2020. As of April 1, 2020, the MMTC license held by McCrory’s is no longer subject to the statutory cap. Through its vertically integrated MMTC license, McCrory’s currently operates 16 medical dispensaries in Florida. |

| (6) | Through its vertically integrated MMTC license, McCrory’s currently operates one co-located cultivation and processing facility located in Lake Wales, Florida. |

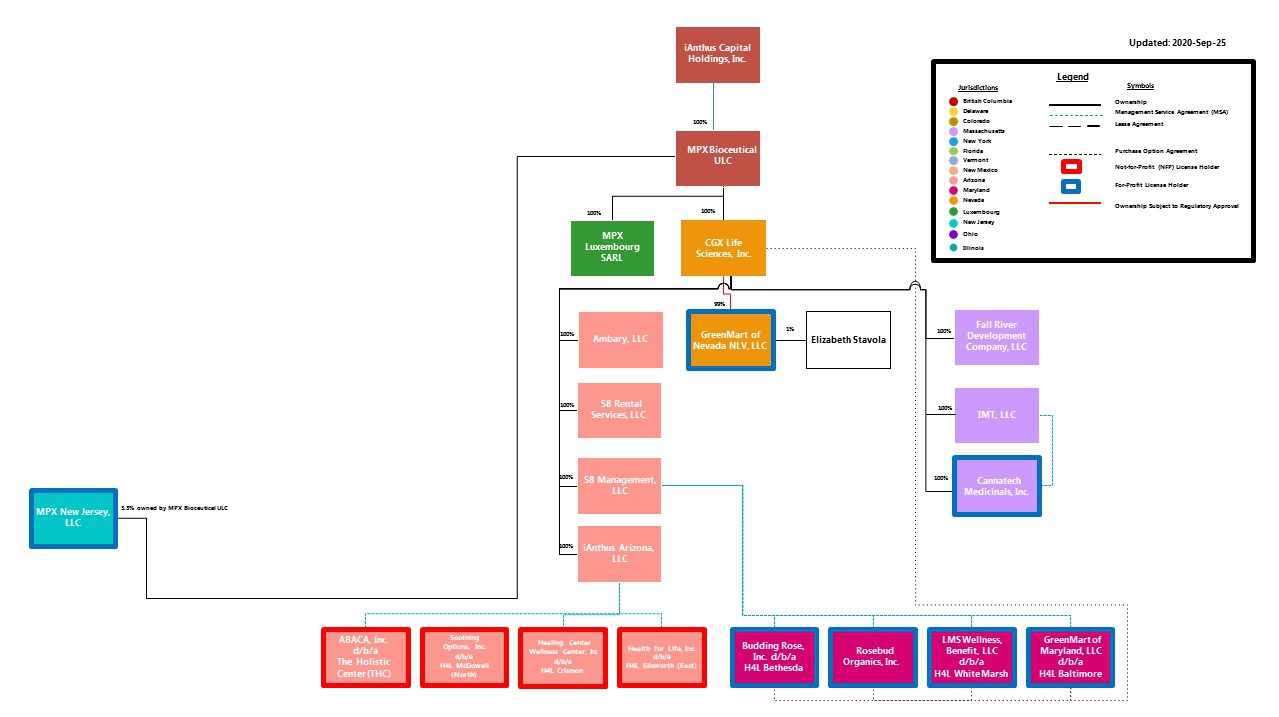

| (7) | Our wholly-owned subsidiary, S8 Management, LLC (“S8 Management”), has entered into management agreements with three medical cannabis dispensaries, LMS, Budding Rose, GMMD and one medical cannabis processor facility, Rosebud. Our wholly-owned subsidiary, CGX Life Sciences, Inc. (“CGX”), holds options to acquire the medical cannabis dispensary licenses and the medical cannabis processor license in the future, subject to regulatory approval. |

| (8) | We, through our wholly-owned subsidiary, iAnthus Capital Management, LLC (“ICM”), own 100% of Mayflower, which holds several medical and adult-use cannabis licenses. In addition, we, through our wholly-owned subsidiary CGX, own 100% of two separate management entities with service and consulting agreements with a second vertically integrated medical cannabis license holder, Cannatech Medicinals, Inc. (“Cannatech”). On October 8, 2020, we obtained approval from the Massachusetts Cannabis Control Commission (“CCC”) to convert Cannatech from a non-profit corporation to a for-profit corporation. On November 16, 2020, Cannatech was converted from a non-profit corporation to a for-profit corporation. As a result of the conversion, Cannatech is now owned 100% by the Company, through its wholly-owned subsidiary, CGX. In Massachusetts, an entity is permitted to control and operate up to three vertically-integrated medical Marijuana Treatment Center licenses, which include medical cultivation, product manufacturing and retail dispensing functions, up to three adult-use Marijuana Establishment cultivation licenses, up to three adult-use Marijuana Establishment product manufacturing licenses and up to three adult-use Marijuana Establishment retail licenses, with a maximum total cultivation “canopy” of up to 100,000 square feet. We, through Mayflower, currently hold one final vertically integrated medical license, one provisional vertically integrated medical license, one final adult-use cultivation license, one final adult-use product manufacturing license, one final adult-use retail license and one provisional adult-use retail license. Mayflower is also currently applying for a third provisional adult-use Marijuana Establishment retail license In addition, Cannatech currently holds one provisional vertically integrated medical license and on October 8, 2020, Cannatech was granted one provisional adult-use Marijuana Establishment cultivation license and one provisional adult-use product manufacturing license. |

| (9) | We currently operate one Marijuana Treatment Center retail location, or medical dispensary, in Boston, Massachusetts. We anticipate operating a total of three medical Marijuana Treatment Center retail locations in Boston, Lowell and Fall River, Massachusetts, subject to applicable regulatory approvals. In addition, we anticipate operating three Marijuana Establishment retail locations, or adult-use dispensaries, two of which we expect will be co-located with our Marijuana Treatment Center retail locations in Boston and Lowell, Massachusetts and one of which will be located in Worcester, Massachusetts, subject to applicable regulatory approvals. On October 8, 2020, we obtained a final license to operate our Worcester, Massachusetts adult-use Marijuana Establishment retail location, which will exclusively maintain adult-use operations and is expected to open in 2020. |

| (10) | Our Holliston, Massachusetts facility currently includes the cultivation and product manufacturing operations of its final vertically integrated medical Marijuana Treatment Center license as well as the operations of its final adult-use Marijuana Establishment cultivation license and product manufacturing license. Subject to regulatory approval, we expect that our Holliston, Massachusetts facility will also include the cultivation and product manufacturing operations of our additional provisional vertically-integrated medical Marijuana Treatment Center license. Subject to regulatory approval, we expect that our Fall River, Massachusetts facility will include the cultivation and product manufacturing operations of the provisional vertically integrated medical Marijuana Treatment Center license held by Cannatech as well as the operations of a provisional adult-use Marijuana Establishment cultivation license and provisional adult-use product manufacturing license granted to Cannatech on October 8, 2020. Subject to applicable regulatory approval, we expect to operate cultivation and product manufacturing functions for three vertically integrated medical licenses, two adult-use cultivation licenses and two adult-use product manufacturing licenses out of two facilities in Holliston and Fall River, Massachusetts. We may also seek an additional adult-use cultivation license and an additional product manufacturing license within the Massachusetts statutory and regulatory limitations. |

-3-

| (11) | As a result of the acquisition of MPX Bioceutical Corporation on February 5, 2019 (the “MPX Acquisition”), we, through our wholly-owned subsidiary CGX, have acquired 99% of the ownership interests of GMNV, a licensed cultivation and production facility located in North Las Vegas, Nevada (the “NLV Facility”) that also holds three conditional dispensary licenses to be located in Henderson, Las Vegas and Reno, Nevada. The change in control of GMNV must be approved by the Nevada Cannabis Compliance Board (“CCB”), which is currently reviewing our application. Approval by the CCB will also result in us acquiring the remaining 1% ownership interest in GMNV and we will then own 100% of GMNV through our wholly-owned subsidiary, CGX. |

| (12) | GMNV currently has two Nevada medical cannabis establishment registration certificates, one for cultivation and one for production, each of which occurs at the NLV Facility. GMNV also currently has two Nevada adult-use licenses, one for cultivation and one for production, each of which also occurs at the same NLV Facility. |

| (13) | On August 27, 2019, iAnthus New Jersey, LLC, our wholly-owned subsidiary, entered into a financing, leasing, licensing and services agreement with MPX NJ, which remains subject to regulatory approval by the New Jersey Department of Health. |

| (14) | One medical dispensary is permitted under the current rules in New Jersey, with the possibility of operating two more satellite dispensaries subject to regulatory approval. Under New Jersey law, the license holder must obtain such approval prior to January 2, 2021. |

| (15) | MPX NJ cultivates medical cannabis at its Pleasantville, New Jersey facility, which is also expected to include processing capabilities. |

| (16) | We, through our wholly-owned subsidiary ICM, own 100% of Citiva, which holds a vertically integrated medical cannabis license allowing Citiva to operate one medical manufacturing facility, including cultivation and processing capabilities and up to four medical dispensaries. Citiva currently operates three medical dispensaries in Brooklyn, Wappingers Falls and Staten Island, New York. We anticipate operating one additional medical dispensary in Ithaca, New York and one manufacturing facility in Warwick, New York, subject to applicable regulatory approvals. |

| (17) | We own 100% of Grassroots Vermont Management Services, LLC (“GVMS”), the sole shareholder of GRVT, which has entered into a management services agreement with GRVT. Accordingly, we, through our wholly-owned subsidiary GVMS, own 100% of GRVT. |

| (18) | GRVT is a Vermont Registered Marijuana Dispensary, which permits GRVT to operate one vertically integrated location to cultivate, process and dispense medical cannabis and one additional dispensing location. GRVT currently operates one vertically integrated location where it cultivates, processes and dispenses medical cannabis in Brandon, Vermont. Subject to regulatory approval, GRVT anticipates opening an additional dispensing location in Burlington, Vermont. |

| (19) | On June 27, 2019, we, through our wholly-owned subsidiary, iA CBD, acquired substantially all of the property and assets of CBD For Life, LLC (“CBD For Life”). As a result of the acquisition of CBD For Life, iA CBD is engaged in the formulation, manufacture, creation and sale of products infused with CBD. The CBD used to manufacture these products is exclusively derived from hemp. We intend for all our hemp-derived products to be produced and sold in accordance with the 2014 Farm Bill and the 2018 Farm Bill, as applicable, at the time and location of operation and for such products to constitute hemp under the 2018 Farm Bill. |

Growth Strategies and Strategic Priorities

Expand retail footprint within existing dispensary license portfolio. We currently have 29 operating dispensaries; however, our licenses permit us to own and/or operate an additional 13 dispensaries in five states, plus an uncapped number of licenses in Florida. We have dispensary licenses in key markets throughout the United States including New York City (Brooklyn and Staten Island), Boston, the Washington D.C. metro area (Bethesda), the Tampa and St. Petersburg area, Phoenix, the Miami and Fort Lauderdale area, Orlando, Baltimore and Las Vegas. We intend to expand our operations in Florida, Massachusetts, Nevada, New Jersey and New York.

Increase cultivation and processing capacity. We have 10 operational cultivation and processing licenses in nine states, with approximately 417,000 square feet of cultivation and processing space which is fully built-out, approximately 400,000 square feet of space which is under construction and the ability to expand to a total of approximately 817,000 square feet of space within our existing lots. We currently have the ability to harvest approximately 56,000 pounds of biomass annually in our existing cultivation space and we believe that we will have the ability to harvest approximately 195,000 pounds of biomass annually if we are able to use all of our projected cultivation space, including the cultivation space that is currently under construction and the additional unused cultivation space within our existing lots.

Increase patient and customer counts per location. We are focused on brand awareness and attracting new and existing patients and customers to our dispensaries and online ordering platforms. Our marketing and sales strategies include medical outreach, industry associations and websites, social media and a variety of other grassroots initiatives.

-4-

Acquire attractive targets to enhance our footprint, product offerings and/or operations. Strategic acquisitions are an important part of our ongoing growth strategy. We expect to continue to make strategic acquisitions that, among other things, are intended to increase revenue, build our geographic footprint, add new branded products to our portfolio and allow us to expand our capabilities and/or help improve operating efficiencies in existing markets.

Secure additional operating licenses throughout the United States. As more states legalize medical and/or adult-use cannabis products or expand their current cannabis regulations, new or additional cultivation, processing and/or dispensary licenses may become available. Given our operational history, we believe that we are well positioned to apply for any such new licenses.

Acquisitions

iA CBD, LLC

On June 27, 2019, we acquired substantially all of the assets and liabilities of CBD For Life through our wholly owned subsidiary, iA CBD, for consideration of $10.9 million (in cash and our common shares). As a result of this acquisition, we entered the CBD products market. We sell CBD For Life products directly to consumers online at www.cbdforlife.us as well as in over 2,300 retail locations across the United States.

MPX Bioceutical ULC

On February 5, 2019, we acquired the U.S. operations of MPX Bioceutical Corporation, which amalgamated into our-wholly owned subsidiary MPX Bioceutical ULC (“MPX”) for consideration of $533.1 million (in our common shares and common shares of a newly formed spin-out corporation which holds all of the non-U.S. cannabis businesses of MPX). In addition, we assumed certain debt instruments, warrants and options of MPX. As a result of the MPX Acquisition, we expanded our operations from six to ten states and added a robust portfolio of MPX-branded products. In addition, we acquired operations in Arizona, Nevada, Maryland and New Jersey and expanded our operations in Massachusetts.

Citiva Medical, LLC

On February 1, 2018, we acquired Citiva which holds one vertically integrated medical cannabis license in the state of New York for consideration of $24.8 million (in cash and our common shares). As a result of the acquisition of Citiva, we expanded our cannabis operations to New York and are permitted to operate one medical manufacturing facility, including cultivation and processing capabilities and up to four medical dispensaries in New York.

GrowHealthy Properties, LLC

On January 17, 2018, we acquired substantially all of the assets of GrowHealthy Properties, LLC (“GHP”) and McCrory’s (collectively “GrowHealthy”) for consideration of $58.3 million (in cash and our common shares). The transactions included the formation of iAnthus Holdings Florida, LLC and GHHIA, each a wholly-owned subsidiary of ICM, together with the purchase of GHP and an option to acquire 100% of McCrory’s for nominal consideration. On September 19, 2019, the option was exercised and 100% of the membership interest in McCrory’s was transferred to GHHIA. As a result of the acquisition of GrowHealthy, we expanded our cannabis operations to Florida and as a result of the acquisition of McCrory’s, we hold a medical marijuana treatment center license in the state of Florida that permits us to operate one or more cultivation and processing facilities and an unlimited number of dispensaries.

-5-

Mayflower and Pilgrim

On December 31, 2017, we acquired an 80% interest in Pilgrim Rock Management, LLC (“Pilgrim”) and on April 17, 2018, we acquired the remaining 20% interest in Pilgrim for consideration of an aggregate of 1,665,734 of our common shares. Pilgrim is an affiliated management company that provides management services, financing, intellectual property licensing, real estate, equipment leasing and certain other services to Mayflower. On July 31, 2018, Mayflower converted from a non-profit into a for-profit corporation and became our wholly-owned subsidiary. As a result of the acquisitions of Mayflower and Pilgrim, we expanded our cannabis operations to Massachusetts. Mayflower maintains one final vertically integrated medical license, one provisional vertically integrated medical license, one final adult-use cultivation license, one final adult-use product manufacturing license, one final adult-use retail license and one provisional adult-use retail license. Mayflower is also currently applying for a third provisional adult-use Marijuana Establishment retail license. Mayflower’s vertically integrated medical Marijuana Treatment Center license is comprised of a co-located cultivation and product manufacturing facility in Holliston, Massachusetts and a dispensary in Boston, Massachusetts, as well as one adult-use Marijuana Establishment cultivation license and one adult-use Marijuana Establishment product manufacturing license, which are also co-located with Mayflower’s medical Marijuana Treatment Center cultivation and product manufacturing facility in Holliston, Massachusetts. Mayflower received its final adult-use Marijuana Establishment retail license for its Worcester, Massachusetts dispensary, which is expected to open before the end of 2020.

Competition

We compete on a state-by-state basis in the limited license medical and adult-use cannabis markets as well as the national CBD markets. Participation in state cannabis programs has significant regulatory and financial hurdles that create high barriers to entry, which result in a limited number of market participants in most states. In addition, most of the states in which we operate impose regulatory limitations on the number of cannabis licenses that can be granted, thus allowing for existing license holders to compete against a fixed number of regulated competitors in a particular market. We face competition from local regulated cannabis operators as well as illicit cannabis businesses and other persons engaging in illicit cannabis-related activities within each state. Our primary competitors include the following multi-state operators: Acreage Holdings, Inc., Cresco Labs Inc., Curaleaf Holdings Inc., Green Thumb Industries Inc., Harvest Health & Recreation, Inc. and Trulieve Cannabis Corp.

With respect to our CBD business, we compete with a growing number of emerging CBD companies including multi-state cannabis operators that also offer CBD products, as well as certain large national and multinational corporations that offer or plan to offer CBD products that are or may be deemed similar to those offered by us.

Recent Developments

Payment of Outstanding Obligations

In connection with the MPX Acquisition, we assumed a long-term note (the “Stavola Trust Note”) in the principal amount of $10.8 million, payable to the Elizabeth Stavola 2016 NV Irrevocable Trust. The trust is for the benefit of Elizabeth Stavola, our former Chief Strategy Officer and a former member of our board of directors (the “Board of Directors” or “Board”). On January 10, 2020, we repaid the outstanding principal amount of $10.8 million and interest of $24,000 on the Stavola Trust Note, repaying the note in full.

-6-

Special Committee Formation

On March 31, 2020, a special committee (the “Special Committee”) comprised of independent directors was formed to launch an investigation into the actions of Hadley Ford, who, at the time of the investigation, was our Chief Executive Officer and a member of the Board. On April 27, 2020, the Special Committee concluded, and our Board accepted, that Mr. Ford entered into two undisclosed loans (one for $100,000 with a related-party and one for $60,000 with a non-arm’s length party) which created a potential or apparent conflict of interest and should have been disclosed to the Board in a timely manner. On that same day, the Board accepted the resignation of Mr. Ford from his positions as a director and officer of the Company as well as from his positions as a director and officer of the Company’s subsidiaries, effective immediately. Immediately following Mr. Ford’s resignation, Randy Maslow, our President, was appointed to serve as our Interim Chief Executive Officer. In connection with Mr. Ford’s resignation, on April 27, 2020, we entered into a settlement and general release agreement with Mr. Ford pursuant to which, among other things, we extended the maturity date of Mr. Ford’s loan to June 30, 2021 and the balance of the loan was partially offset by compensation owed to Mr. Ford in the amount of $488,467.

Financial Restructuring

Due to the liquidity constraints we experienced in the first quarter of 2020, we attempted to negotiate temporary relief of our interest obligations with the holders (the “Secured Lenders”) of our 13% senior secured convertible debentures (the “Secured Convertible Notes”) issued by ICM. However, we were unable to reach an agreement and did not make interest payments when due and payable to the Secured Lenders or payments that were due to the holders of our 8% convertible unsecured debentures (the “Unsecured Convertible Debentures” and together with the Secured Convertible Notes, the “Debentures”) (the “Unsecured Lenders” and together with the Secured Lenders, the “Lenders”). As of September 30, 2020, we are in default of our obligations pursuant to the Debentures which consists of $97,507,778 and $60,000,000 in principal amount plus accrued interest thereon with respect to the Secured Convertible Notes and Unsecured Convertible Debentures, respectively.

As a result of the default, all amounts, including principal and accrued interest, became immediately due and payable to the Lenders. Furthermore, as a result of the default, we also became obligated to pay an exit fee (the “Exit Fee”) of $10,000,000 that accrues interest at a rate of 13% annually in relation to the Secured Convertible Notes, which, as of September 30, 2020, is in excess of approximately $12.9 million. Upon payment of the Exit Fee, the holders of the Secured Convertible Notes issued in May 2018 (“Tranche One Secured Convertible Notes”) are required to transfer the 3,891,051 common shares issued under the $10,000,000 equity financing that closed concurrently with the Tranche One Secured Convertible Notes to us. As of September 30, 2020, we have not paid the Exit Fee and such shares have not been transferred to us.

On June 22, 2020, we received a notice demanding repayment under the Secured Notes Purchase Agreement of the entire principal amount of the Secured Convertible Notes, together with interest, fees, costs and other charges that have accrued or may accrue from Gotham Green Admin 1, LLC, the collateral agent (the “Collateral Agent”) holding security for the benefit of the Secured Convertible Notes. The Collateral Agent concurrently provided us with a Notice of Intention to Enforce Security under section 244 of the Bankruptcy and Insolvency Act (Canada) (the “BIA Notice”). Pursuant to section 244 of the Bankruptcy and Insolvency Act (Canada) (the “BIA”), the Collateral Agent may not enforce the security over the collateral granted by us until ten days after sending the BIA Notice unless we consent to an earlier enforcement of the security.

-7-

On July 13, 2020, we entered into a restructuring support agreement (the “Restructuring Support Agreement”) with the Secured Lenders and a majority of the Unsecured Lenders (the “Consenting Unsecured Lenders”) to effectuate a proposed recapitalization transaction (“the Recapitalization Transaction”) to be implemented by way of a court-approved plan of arrangement (the “Plan of Arrangement”) under the Business Corporations Act (British Columbia) (the “BCBCA”) following approval by the Secured Lenders, Unsecured Lenders and our existing shareholders. Pursuant to the Recapitalization Transaction, the Secured Lenders, the Unsecured Lenders and our shareholders are to be allocated and issued, approximately, such amounts of Restructured Senior Debt (as defined below), Interim Financing (as defined below), 8% Senior Unsecured Convertible Debentures and percentage of our pro forma common shares, as presented in the following table:

| (in ’000s of U.S. dollars) | Restructured Senior Debt(1) | Interim Financing(2) | 8% Senior Unsecured Debentures(3) | Pro Forma Common Equity(4) | ||||||||||||

| Secured Lenders | $ | 85,000 | $ | 14,737 | $ | 5,000 | 48.625 | % | ||||||||

| Unsecured Lenders | - | - | 15,000 | 48.625 | % | |||||||||||

| Existing Shareholders | - | - | - | 2.75 | % | |||||||||||

| Total | $ | 85,000 | $ | 14,737 | $ | 20,000 | 100.00 | % | ||||||||

| (1) | The principal balance of the Secured Convertible Notes will be reduced to $85,000,000, which will be increased by the amount of the Interim Financing, which has a first lien, senior secured position over all of our assets, is non-convertible and non-callable for three years and includes payment in kind at an interest rate of 8% per year and a maturity date which will be five years after the consummation of the Recapitalization Transaction (the “Restructured Senior Debt”). |

| (2) | The Secured Lenders provided $14,736,842 of Interim Financing to ICM, on substantially the same terms as the Restructured Senior Debt, net of a 5% original issue discount. The amounts of the Interim Financing along with any accrued interest thereon is expected to be converted into, and the original principal balance will be added to, the Restructured Senior Debt upon consummation of the Recapitalization Transaction. |

| (3) | The 8% Senior Unsecured Debentures include payment in kind at an interest rate of 8% per year, a maturity date which will be five years after the consummation of the Recapitalization Transaction, are non-callable for three years and are subordinate to the Restructured Senior Debt but senior to our common shares. |

| (4) | Following consummation of the Recapitalization Transaction, a to-be-determined amount of equity will be made available for management, employee and director incentives, as determined by the New Board (as defined below). All of our existing warrants and options will be cancelled and our common shares may be consolidated pursuant to a consolidation ratio which has yet to be determined. |

Upon consummation of the Recapitalization Transaction, a new board of directors (the “New Board”) will be composed of the following members: (i) three nominees will be designated by the Secured Lenders; (ii) three nominees will be designated by the Consenting Unsecured Lenders; and (iii) one nominee will be designated by the director nominees of the Secured Lenders and Consenting Unsecured Lenders to serve as a member of our Board of Directors.

Pursuant to the terms of the proposed Recapitalization Transaction, the Collateral Agent, the Secured Lenders and the Consenting Unsecured Lenders agreed to forbear from further exercising any rights or remedies in connection with any events of default that now exist or may in the future arise under any of the purchase agreements with respect of the Secured Convertible Notes and all other agreements delivered in connection therewith, the purchase agreements with respect of the Unsecured Convertible Debentures and all other agreements delivered in connection therewith and any other agreement to which the Collateral Agent, Secured Lenders, or Consenting Unsecured Lenders are a party to (collectively, the “Defaults”) and shall take such steps as are necessary to stop any current or pending enforcement efforts in relation thereto. Upon consummation of the Recapitalization Transaction, the Collateral Agent, Secured Lenders and Consenting Unsecured Lenders are also expected to irrevocably waive all Defaults and take all steps required to withdraw, revoke and/or terminate any enforcement efforts in relation thereto.

On September 14, 2020, our securityholders voted in support of the Recapitalization Transaction. Specifically, all of the holders of the Secured Convertible Notes and Unsecured Convertible Debentures voted in favor of the Plan of Arrangement. In addition, the holders of our common shares, options and warrants, representing 79.0% of the votes cast, voted in favor of the Plan of Arrangement.

On October 5, 2020, the Plan of Arrangement was approved by the Supreme Court of British Columbia, subject to the receipt of all necessary regulatory and stock exchange approvals.

-8-

On November 3, 2020, Walmer Capital Limited, Island Investments Holdings Limited and Alastair Crawford collectively served and filed a Notice of Appeal with respect to the Court’s approval of the Plan of Arrangement.

Financing

On July 13, 2020, ICM issued secured debentures (“July Secured Debentures”) in the aggregate principal amount of $14,736,842 (including a 5% original issue discount) to the Secured Lenders pursuant to a Second Amended and Restated Debenture Purchase Agreement dated as of July 10, 2020 and as contemplated pursuant to the Recapitalization Transaction. The July Secured Debentures mature on July 13, 2025 and accrue interest at a rate of 8% annually. Interest is to be paid in kind by adding the interest accrued to the principal amount on the last day of each fiscal quarter and thereafter such added amount will become part of the principal amount and will begin to accrue interest at a rate of 8% annually. Interest will be payable on the date that all of the principal amount is due and payable. ICM is not permitted to redeem, convert, or prepay the July Secured Debentures prior to July 13, 2023 without the prior written consent of the Secured Lenders. Similar to the Secured Notes, the July Secured Debentures are secured by certain of our current and future assets.

Mutual Termination of Acquisition

On July 31, 2020, we and WSCC, Inc. (“Sierra Well”) announced the mutual termination of the previously announced merger agreement entered into on September 18, 2019 pursuant to which we were to acquire Sierra Well, a cannabis cultivator, processor, distributor and retailer in Nevada subject to regulatory approval.

Redemption of 24.6% Equity Interest in RGA

On October 22, 2020, our 24.6% equity interest in RGA was redeemed for approximately $2.4 million. RGA is owned in part by an individual with a familial relationship to Hadley Ford, our former officer and director.

Intellectual Property

Our portfolio of subsidiaries currently includes a number of local brands; however, we intend to transition to a national model under fewer brands. As cannabis currently remains illegal under U.S. federal law, we cannot register our cannabis brands with the U.S. Patent and Trademark Office (“USPTO”). However, we rely on the intellectual property protections afforded under applicable state laws and common law through the use of our marks in commerce in each of the respective regions in which we operate.

Governmental Regulations

Cannabis

In the United States, the cultivation, manufacturing, importation, distribution, use and possession of cannabis is illegal under U.S. federal law. However, medical and adult-use cannabis has been legalized and regulated by individual states. Currently, 36 states plus the District of Columbia and certain U.S. territories recognize, in one form or another, the medical use of cannabis, while 15 of those states plus the District of Columbia and certain U.S. territories recognize, in one form or another, the full adult-use of cannabis. Notwithstanding the regulatory environment with respect to cannabis at the state level, cannabis continues to be categorized as a Schedule I controlled substance under the U.S. Controlled Substances Act (the “CSA”). Accordingly, the use, possession, or distribution of cannabis violates U.S. federal law. As a result, cannabis businesses in the United States are subject to inconsistent state and federal legislation, regulation and enforcement.

-9-

Under former President Barack Obama, in an effort to provide guidance to U.S. federal law enforcement regarding the inconsistent regulation of cannabis at the U.S. federal and state levels, the U.S. Department of Justice (“DOJ”) released a memorandum on August 29, 2013 titled “Guidance Regarding Marijuana Enforcement” from former Deputy Attorney General James Cole (the “Cole Memorandum”). The Cole Memorandum acknowledged that, although cannabis is a Schedule I controlled substance under the CSA, the U.S. Attorneys in states that have legalized cannabis should prioritize the use of the U.S. federal government’s limited prosecutorial resources by focusing enforcement actions on the following eight areas of concern (the “Cole Priorities”):

| ● | Preventing the distribution of marijuana to minors; | |

| ● | Preventing revenue from the sale of marijuana from going to criminal enterprises, gangs and cartels; | |

| ● | Preventing the diversion of marijuana from states where it is legal under state law in some form to other states; | |

| ● | Preventing state-authorized marijuana activity from being used as a cover or pretext for the trafficking of other illegal drugs or other illegal activity; | |

| ● | Preventing violence and the use of firearms in the cultivation and distribution of marijuana; | |

| ● | Preventing drugged driving and the exacerbation of other adverse public health consequences associated with marijuana use; | |

| ● | Preventing the growing of marijuana on public lands and the attendant public safety and environmental dangers posed by marijuana production on public lands; and | |

| ● | Preventing marijuana possession or use on U.S. federal property. |

In January 2018, under the administration of President Donald Trump, former U.S. Attorney General Jeff Sessions rescinded the Cole Memorandum. While this did not create a change in U.S. federal law, as the Cole Memorandum was policy guidance and not law, the rescission added to the uncertainty of U.S. federal enforcement of the CSA in states where cannabis use is legal and regulated. Former Attorney General Sessions, concurrent with the rescission of the Cole Memorandum, issued a memorandum (“Sessions Memorandum”) which explained that the Cole Memorandum was “unnecessary” due to existing general enforcement guidance adopted in the 1980s, as set forth in the U.S. Attorney’s Manual (“USAM”). The USAM enforcement priorities, like those of the Cole Memorandum, are also based on the U.S. federal government’s limited resources and include law enforcement priorities set by the Attorney General, the seriousness of the alleged crimes, the deterrent effect of criminal prosecution and the cumulative impact of particular crimes on the community.

While the Sessions Memorandum emphasizes that cannabis is a Schedule I controlled substance under the CSA and states that it is a “dangerous drug and that marijuana activity is a serious crime,” it does not otherwise provide that the prosecution of cannabis-related offenses is now a DOJ priority. Furthermore, the Sessions Memorandum explicitly indicates that it is a guide for prosecutorial discretion and that discretion is firmly in the hands of U.S. Attorneys who determine whether to prosecute cannabis-related offenses. U.S. Attorneys could individually continue to exercise their discretion in a manner similar to that permitted under the Cole Memorandum. While certain U.S. Attorneys have publicly affirmed their commitment to proceeding in a manner contemplated under the Cole Memorandum, or otherwise affirmed that their views of U.S. federal enforcement priorities have not changed as a result of the rescission of the Cole Memorandum, others have publicly supported the rescission of the Cole Memorandum.

As of the date of hereof, although the Department of Justice under Attorney General William Barr has not taken a formal position on the federal enforcement of laws relating to cannabis, Attorney General William Barr stated that his preference would be to have a uniform federal rule against cannabis, but, absent such a uniform rule, his preference would be to permit the existing federal approach leaving it up to the states to make their own decision. In addition, Attorney General William Barr has indicated that the DOJ is currently reviewing the Strengthening the Tenth Amendment Through Entrusting States Act (“STATES Act”), which would shield individuals and businesses complying with state cannabis laws from federal intervention.

-10-

Other federal legislation provides or seeks to provide protection to individuals and businesses acting in violation of U.S. federal law but in compliance with state cannabis laws. For example, the Rohrabacher-Farr Amendment has been included in annual spending bills passed by Congress since 2014. The Rohrabacher-Farr Amendment restricts the DOJ from using federal funds to interfere with states implementing laws that authorize the use, distribution, possession, or cultivation of medical cannabis.

U.S. courts have construed these appropriations bills to prevent the U.S. federal government from prosecuting individuals or businesses engaged in cannabis-related activities to the extent they are operating in compliance with state medical cannabis laws. However, because this conduct continues to violate U.S. federal law, U.S. courts have observed that should the U.S. Congress choose to appropriate funds to prosecute individuals or businesses acting in violation of the CSA, such individuals or businesses could be prosecuted for violations of U.S. federal law even to the extent/even if they are operating in compliance with applicable state medical cannabis laws.

If Congress declines to include the Rohrabacher-Farr Amendment in future fiscal year appropriations bills or fails to pass necessary budget legislation causing a government shutdown, the U.S. federal government will have the authority to spend federal funds to prosecute individuals and businesses acting contrary to the CSA for violations of U.S. federal law.

Furthermore, the appropriations protections only apply to individuals and businesses operating in compliance with a state’s medical cannabis laws and provide no protection to individuals or businesses operating in compliance with a state’s adult-use cannabis laws. On June 20, 2019, however, the U.S. House of Representatives passed the Blumenauer-Norton-McClintock Amendment, which would expand the protections afforded by the Rohrabacher-Farr Amendment to individuals and businesses operating in compliance with applicable state adult-use cannabis laws. The U.S. Senate did not include the Blumenauer-McClintock-Norton Amendment in its appropriations bill, and ultimately, the Blumenauer-McClintock-Norton Amendment was not passed into law. On July 30, 2020, the U.S. House of Representatives again voted to include the Blumenauer-Norton-McClintock Amendment in the Commerce, Justice, Science and Related Agencies Appropriations Act, 2021. However, it is unclear whether the U.S. Senate will include the Blumenauer-McClintock-Norton Amendment in its version of the appropriations bill and whether it will ultimately be included in appropriations legislation for 2021.

Additionally, there are a number of marijuana reform bills that have been introduced in the U.S. Congress that would amend federal law regarding the legal status and permissibility of medical and adult-use cannabis, including the STATES Act, the Marijuana Opportunity Reinvestment and Expungement Act (the “MORE Act”) and the Substance Regulation and Safety Act (the “SRSA”). The STATES Act would create an exemption in the CSA to allow states to determine their own cannabis policies without fear of federal reprisal. The MORE Act, which was passed by the House Judiciary Committee on November 20, 2019, would remove cannabis from the CSA, expunge federal cannabis offenses and establish a 5% excise tax on cannabis to fund various federal grant programs. The SRSA, which was introduced by U.S. Senator Tina Smith on July 30, 2020, would remove cannabis from the CSA, grant the FDA authority to regulate cannabis and cannabis products and regulate the safety and quality control of cannabis crops and the import and export of cannabis materials. On December 4, 2020, the House passed the MORE Act. Nevertheless, it is uncertain which federal marijuana reform bills, if any, will ultimately be passed and signed into law.

-11-

Businesses in the regulated cannabis industry, including our business, are subject to a variety of laws and regulations in the United States that involve money laundering, financial recordkeeping and proceeds of crime, including the U.S. Currency and Foreign Transactions Reporting Act of 1970 (“Bank Secrecy Act”) and the Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act (the “US PATRIOT Act”) and the rules and regulations thereunder and any related or similar rules, regulations, or guidelines, issued, administered, or enforced by governmental authorities in the United States. Further, under U.S. federal law, banks or other financial institutions that provide a cannabis business with a checking account, debit or credit card, small business loan, or any other service could be charged with money laundering, aiding and abetting, or conspiracy.

Despite these laws, the Financial Crimes Enforcement Network (“FinCEN”), a bureau within the U.S. Department of the Treasury (“U.S. Treasury”), issued a memorandum on February 14, 2014 (the “FinCEN Memorandum”), which provides instructions to banks and other financial institutions seeking to provide services to cannabis-related businesses. The FinCEN Memorandum explicitly references the Cole Priorities and indicates that in some circumstances it is permissible for banks and other financial institutions to provide services to cannabis-related businesses without risking prosecution for violation of U.S. federal money laundering laws. Under these guidelines, financial institutions are subject to a requirement to submit a suspicious activity report in certain circumstances as required by federal money laundering laws. These cannabis related suspicious activity reports are divided into three categories: marijuana limited, marijuana priority and marijuana terminated, based on the financial institution’s belief that the marijuana business follows state law, is operating out of compliance with state law, or where the banking relationship has been terminated, respectively. The FinCEN Memorandum refers to supplementary guidance in the Cole Memorandum relating to the prosecution of money laundering offenses predicated on cannabis-related violations of the CSA.

The rescission of the Cole Memorandum did not affect the status of the FinCEN Memorandum, and to date, the U.S. Treasury has not given any indication that it intends to rescind the FinCEN Memorandum. While the FinCEN Memorandum was originally intended to work in tandem with the Cole Memorandum, the FinCEN Memorandum appears to remain in effect as standalone guidance. Although the FinCEN Memorandum remains intact, indicating that the U.S. Treasury and FinCEN intend to continue abiding by its guidance, it is unclear whether the Trump administration will continue to follow the guidelines set forth under the FinCEN Memorandum.

In March 2019, the U.S. House of Representatives Financial Services Committee passed the Secure and Fair Enforcement Banking Act (the “SAFE Banking Act”) and the U.S. Senate held a hearing on the SAFE Banking Act in July 2019. On September 25, 2019, the U.S. House of Representatives passed the SAFE Banking Act. The SAFE Banking Act creates protections for financial institutions that provide banking services to businesses acting in compliance with applicable state cannabis laws, but it is uncertain whether it will be passed by the U.S. Senate and ultimately signed into law. On May 15, 2020, the U.S. House of Representatives passed the Health and Economic Recovery Omnibus Emergency Solutions Act (the “HEROES Act”), which included the provisions of the SAFE Banking Act. The U.S. House of Representatives passed a more limited version of the HEROES Act on October 1, 2020, which also includes the provisions of the SAFE Banking Act. However, it is unclear whether the version of the HEROES Act to be passed by the U.S. Senate and ultimately signed into law will include the provisions of the SAFE Banking Act.

There can be no assurance that state laws legalizing and regulating the sale and use of cannabis will not be repealed or overturned or that local governmental authorities will not limit the applicability of state laws within their respective jurisdictions. In addition, local and city ordinances may strictly limit and/or restrict the distribution of cannabis in a manner that could make it difficult or impossible to operate cannabis businesses in certain jurisdictions.

-12-

Hemp

On December 20, 2018, the U.S. Agriculture Improvement Act of 2018 (the “2018 Farm Bill”) was signed into law. Prior to its enactment, the U.S. federal government did not distinguish between cannabis and hemp and the entire plant species Cannabis sativa L. (subject to narrow exceptions applicable to specific portions of the plant) was scheduled as a controlled substance under the CSA. Therefore, the cultivation of hemp for any purpose in the United States without a Schedule I registration with the U.S. Drug Enforcement Agency (“DEA”) was federally illegal, unless exempted by Section 7606 of the Agricultural Act of 2014 (the “2014 Farm Bill”). The 2018 Farm Bill removed hemp (which is defined as “the plant Cannabis sativa L. and any part of that plant, including the seeds thereof and all derivatives, extracts, cannabinoids, isomers, acids, salts and salts of isomers, whether growing or not, with a delta-9 tetrahydrocannabinol concentration of not more than 0.3 percent on a dry weight basis”) and its derivatives, extracts and cannabinoids, including cannabidiol (“CBD”) derived from hemp, from the definition of marijuana in the CSA, thereby removing hemp and its derivatives from DEA purview as a controlled substance. The 2018 Farm Bill also amends the Agricultural Marketing Act of 1946 to allow for the commercial production of hemp in the United States under the purview of the United States Department of Agriculture (the “USDA”) in coordination with state departments of agriculture that elect to have primary regulatory authority over hemp production in their respective jurisdictions. Pursuant to the 2018 Farm Bill, states, U.S. territories and tribal governments may adopt their own regulatory plans for hemp production even if more restrictive than federal regulations so long as they meet minimum federal standards and are approved by the USDA. Hemp production in states and tribal territories that do not choose to submit their own plans and that do not prohibit hemp production will be governed by USDA regulation.

On October 31, 2019, the USDA issued an interim final rule governing the domestic production of hemp under the 2018 Farm Bill, establishing the U.S. Domestic Hemp Production Program (the “USDA IFR”). The USDA IFR will be effective from October 31, 2019 through November 1, 2021, at which time the USDA may adopt permanent regulations. The USDA IFR outlines the requirements for the USDA to approve plans submitted by states and tribal governments for the domestic production of hemp. It also establishes a federal plan for hemp producers in states or territories of Native American tribes that do not have USDA-approved hemp production plans. Pursuant to the USDA IFR, the USDA reviews hemp production plans submitted by state and tribal governments that wish to obtain or retain primary regulatory authority over hemp production in their respective jurisdictions. Once the USDA formally receives a plan from a state or tribal government, the agency has 60 days to review and approve or reject the plan.

Although the USDA IFR provides the framework for the USDA, state departments of agriculture and tribal governments to begin the implementation of commercial hemp production programs pursuant to the 2018 Farm Bill, the 2014 Farm Bill was scheduled to remain in effect for one year after the effective date of the USDA IFR.

Accordingly, until the USDA approves a state or tribal hemp production plan and licenses are issued pursuant to a USDA-approved plan, the 2014 Farm Bill is currently the primary U.S. federal law governing domestic hemp production. The application of the hemp provisions of the 2014 Farm Bill was set to expire on October 31, 2020, at which time state programs would be required to comply with the 2018 Farm Bill regulations. However, with this deadline approaching, U.S. Senators and state agricultural departments requested an extension of the application of the 2014 Farm Bill and a delay of the implementation of the 2018 Farm Bill due to delays caused by COVID-19. On October 1, 2020, a Continuing Resolution passed by the U.S. House of Representatives and U.S. Senate was signed by President Trump to fund federal agencies at fiscal 2020 levels through December 11, 2020, which also extended the application of the hemp provisions of the 2014 Farm Bill and delayed the implementation of the 2018 Farm Bill for another year until October 31, 2021.

-13-

Under both the 2014 Farm Bill and the 2018 Farm Bill, states and tribal governments have authority to adopt regulatory regimes that are more restrictive than federal mandates or prohibit hemp production altogether. Accordingly, variance in hemp regulation across jurisdictions is likely to persist. Compliance with state hemp law, if any, is required under both the 2014 Farm Bill and 2018 Farm Bill.

As a result of the 2018 Farm Bill, federal law now provides that CBD derived from hemp is not a controlled substance under the CSA; however, CBD derived from hemp could still be considered a controlled substance under applicable state law. States take varying approaches to regulating the production and sale of hemp and hemp-derived CBD. While some states explicitly authorize and regulate the production and sale of CBD or otherwise provide legal protection for authorized individuals and businesses to engage in commercial hemp activities, other states maintain outdated drug laws that do not distinguish hemp or hemp-derived CBD from marijuana (or “cannabis” as used herein), resulting in hemp being classified as a controlled substance under certain state laws. In these states, the sale of CBD, notwithstanding its origin, is either restricted to state medical or adult-use cannabis program licensees or remains unlawful. Additionally, a number of states prohibit the sale of consumable CBD products based on the position of the U.S. Food and Drug Administration (the “FDA”) set forth in the Federal Food, Drug & Cosmetic Act (the “FFDCA”) that it is unlawful to introduce food containing added CBD or THC into interstate commerce, or to market CBD or THC products as or in dietary supplements regardless of whether the substances are hemp-derived.

The 2018 Farm Bill preserves the authority and jurisdiction of the FDA under the FFDCA to regulate the manufacture, marketing and sale of food, drugs, dietary supplements and cosmetics, including products that contain hemp extracts and derivatives such as CBD. As a producer and marketer of hemp-derived products, we are required to comply with FDA regulations applicable to the manufacturing and marketing of such products, including with respect to dietary supplements, food and cosmetics. To date, the FDA has not deemed CBD or other cannabinoids permissible for use in dietary supplements, as dietary ingredients, or as safe for use in food. The FDA has consistently taken the position that CBD is prohibited from being marketed as a dietary supplement or added to food because substantial clinical trials studying CBD as a new drug were made public prior to the marketing of any food or dietary supplements containing CBD.

To date, the FDA has issued warning letters to companies unlawfully marketing CBD products. In many of these cases, the manufacturer made unsubstantiated claims that products containing CBD are able to treat serious medical conditions, including cancer, Alzheimer’s disease, opioid withdrawal and anxiety, among others, without obtaining drug approvals. Some of these letters were co-signed with the U.S. Federal Trade Commission and cited the companies for making claims about the efficacy of CBD that were not substantiated by scientific evidence.

The FDA has stated that it recognizes the potential opportunities and significant interest in drugs and consumer products containing CBD, is committed to evaluating the agency’s regulatory policies related to CBD and has established a high-level internal working group to explore potential pathways for various types of CBD products to be lawfully marketed. The FDA has authority to issue regulation that would allow these naturally-occurring hemp compounds to be added to food or dietary supplements. In May 2019, the FDA held a public hearing to obtain scientific data and information about the safety, manufacturing, product quality, marketing, labeling and sale of products containing cannabis or cannabis-derived compounds.

-14-

In connection with the Further Consolidated Appropriations Act, 2020, the House Committee on Appropriations issued an explanatory statement agreeing to appropriate $2 million in funding to the FDA for research, policy evaluation, market surveillance and issuance of an enforcement discretion policy for products under the FDA’s jurisdiction that contain CBD. The legislation requires the FDA to provide a report within 60 days regarding its progress in obtaining and analyzing data to help determine a policy of enforcement discretion and the process through which CBD will be evaluated for use in products. On March 5, 2020, the FDA issued a report on its progress and committed to expanding its educational efforts regarding CBD products, encouraging, facilitating and initiating more research on CBD, continuing to monitor the CBD marketplace and take appropriate action against unlawful CBD products that pose a risk of harm to the public and developing a risk-based enforcement policy aimed at protecting the public and providing more regulatory clarity regarding the FDA’s CBD enforcement priorities. The FDA further announced that it is actively evaluating potential rulemaking to allow CBD in dietary supplements. The FDA is also required to conduct a sampling study of the current CBD marketplace to determine the extent to which products containing CBD are mislabeled or adulterated within 180 days of the enactment of the Further Consolidated Appropriations Act, 2020.

On July 9, 2020, the FDA issued its sampling study to the U.S. House Committee on Appropriations and the U.S. Senate Committee on Appropriations detailing the sampling conducted in recent years on CBD products. While the minority of CBD products previously tested by the FDA contained CBD concentrations consistent with their labeling, the report states that a majority of products tested for potentially harmful elements “did not raise significant public health concerns.” The report further provides that the FDA will undertake a more extensive sampling effort expected to cover a representative sample of currently marketed CBD products, including tinctures, oils, extracts, capsules, powders, gummies, water and other beverages, conventional foods, cosmetics, lubricants, tampons, suppositories, vape cartridges and products sold for consumption by pets. Products will be evaluated for cannabinoid content as well as potentially harmful elements.

The rules, regulations and enforcement in this area continue to evolve and develop. Most recently, on August 20, 2020, the DEA issued an interim final rule conforming its regulations to the 2018 Farm Bill (the “DEA IFR”), which went into effect on August 21, 2020. The DEA IFR was subject to public comment through October 20, 2020, which period has since expired. Notably, the DEA IFR creates uncertainty with respect to the federal legal status of any hemp derivative, extract, or product that exceeds a delta-9 tetrahydrocannabinol concentration of 0.3 percent during processing, which, pursuant to the DEA IFR, renders it a federal Schedule I substance under the CSA even if the hemp plant from which any such material is sourced does not exceed the 0.3 percent threshold.

Additionally, on September 4, 2020, the Hemp and Hemp-Derived CBD Consumer Protection and Market Stabilization Act of 2020 was introduced in the U.S. House of Representatives, which permits the inclusion of hemp and CBD derived from hemp as ingredients in dietary supplements that otherwise comply with the applicable requirements for dietary supplements set forth in the FFDCA and the Fair Packaging and Labeling Act. The bill does not address the inclusion of hemp or CBD derived from hemp as ingredients in food products, and it is unclear whether it will ultimately be passed and signed into law.

The rules, regulations and enforcement in this area continue to evolve and develop. Until the FDA formally adopts regulations authorizing the production and sale of CBD products as food and/or dietary supplements, there is a risk that the FDA could take enforcement action against us. Failure to comply with FDA requirements may result in, among other things, warning letters, injunctions, product withdrawals, recalls, seizures, fines and criminal prosecutions. We continue to closely monitor FDA developments with respect to CBD and our compliance with applicable United States laws relating to hemp, including the FDA’s regulations of CBD and evaluate and implement appropriate compliance measures on an ongoing basis.

Application of Cannabis Regulations in the United States

Violations of U.S. federal laws and regulations could result in significant fines, penalties, administrative sanctions, convictions, or settlements arising from either civil or criminal proceedings brought by either the U.S. federal government or private citizens, including, but not limited to, disgorgement of profits, seizure of property or products, cessation of business activities, or divestiture. Our cannabis business activities and the cannabis business activities of our subsidiaries, while believed to be compliant with applicable U.S. state and local laws, currently are illegal under U.S. federal law.

-15-

Cannabis regulations in Canada

We do not, directly or indirectly, engage in the cultivation, processing, or dispensing of cannabis or any other cannabis-related activity in Canada. As such, to our knowledge, our Canadian corporate operations are not subject to any cannabis regulations in Canada.

Employees

As of September 30, 2020, we have 663 full-time and 170 part-time employees. We are not a party to any collective bargaining agreements. We believe that we maintain good relations with our employees.

Corporate Information

We are a company incorporated under the laws of British Columbia, Canada. We were incorporated on November 15, 2013 under the name Genarca Holdings Ltd. and on August 4, 2016, we changed our name to iAnthus Capital Holdings, Inc.

Our corporate headquarters is located at 420 Lexington Avenue, Suite 414, New York, NY 10170 and our telephone number is (646) 518-9411. Our website address is www.ianthus.com. No information available on or through our website shall be deemed to be incorporated into this Registration Statement on Form 10.

Our common shares, no par value, are listed on the Canadian Securities Exchange (“CSE”) under the symbol “IAN” and quoted on the OTC Pink Tier of the OTC Markets Group, Inc. under the symbol “ITHUF.”

ITEM 1A. RISK FACTORS.

Risk Factors Related to Our Company

We rely on third-party suppliers, manufacturers and contractors.

We rely on third-party suppliers, manufacturers and contractors to provide certain products and services. Due to the uncertain regulatory landscape for regulating cannabis in the United States, our third-party suppliers, manufacturers and contractors may elect, at any time, to decline or withdraw services necessary for our operations and the operations of our subsidiaries. Loss of these suppliers, manufacturers and contractors could have a material adverse effect on our business, financial condition and results of operations.

We may not be able to continue executing our merger and acquisition strategy successfully.

Our business plan depends in part on our ability to continue merging with or acquiring other businesses in the cannabis industry, including cultivators, processors, manufacturers and dispensaries. The success of any acquisition will depend upon, among other things, our ability to integrate acquired personnel, operations, products and technologies into our organization effectively, to retain and motivate key personnel of acquired businesses, to retain their customers and maintain product quality.

-16-

Any future mergers or acquisitions, or similar transactions, are subject to conditions, which may include, without limitation, our satisfactory completion of due diligence, negotiation and finalization of formal legal documents, financing and approval from our Board of Directors. As a result, there can be no assurance that we will complete any such transactions. If we do not complete such transactions, we may be subject to a number of risks, including, but not limited to:

| ● | a decline in the price of our common shares to the extent that the current market price reflects a market assumption that these transactions will be completed; |

| ● | the payment of certain costs related to each transaction, such as legal, accounting and consulting fees, even if a transaction is not completed; and |

| ● | an absence of assurance that such opportunities will be available to us in the future, or at all. |

Furthermore, any future merger or acquisition may result in the diversion of management’s attention from other business concerns. In addition, such transactions may be dilutive to our financial results and/or result in impairment charges and write-offs. Such transactions could involve other risks, including the assumption of unidentified or unknown liabilities, disputes or contingencies, for which we, as a successor owner, may be responsible, and/or changes in the industry, location, or regulatory or political environment in which these investments are located, that our due diligence review may not adequately uncover and that may arise after entering into such transactions.

Although we expect to realize strategic, operational and financial benefits as a result of our mergers and acquisitions, we cannot predict whether and to what extent such benefits will be achieved.

We compete for market share with other companies, which may have longer operating histories, more financial resources and more manufacturing and marketing experience than us.

We face and expect to continue to face, competition from other companies some of which may have longer operating histories, more financial resources, more experience and greater brand recognition than us. Increased competition by larger and well-financed competitors and/or competitors that have longer operating histories, greater brand recognition and more manufacturing and marketing experience than us could have a material adverse effect on our business, financial condition and results of operations. As we operate in an early stage industry, we expect to face additional competition from new entrants. Specifically, we expect to face additional competition from new market entrants that are granted licenses within a particular state in which we operate or existing license holders which are not yet active in the industry. If a significant number of new licenses are granted, we may experience increased competition for market share and downward price pressure on our products as new entrants increase production, which could have a material adverse effect on our business.

In addition, if the number of users of cannabis increases, the demand for products will increase and we expect that competition will become more intense, as current and future competitors begin to offer an increasing number of diversified products. To remain competitive, we will require a continued high level of investment in research and development together with marketing, sales and other support. We may not have sufficient resources to maintain research and development and sales efforts on a competitive basis, which could have a material adverse effect on our business, financial condition and results of operations.

-17-

Our U.S. tax classification could have a material adverse effect on our financial condition and results of operations.

Although we are a Canadian corporation, we are classified as a U.S. domestic corporation for U.S. federal income tax purposes under section 7874(b) of the U.S. Internal Revenue Code of 1986, as amended (the “U.S. Tax Code”) and will be subject to U.S. federal income tax on our worldwide income. However, for Canadian tax purposes, regardless of any application of section 7874 of the U.S. Tax Code, we are treated as a Canadian resident corporation. As a result, we are subject to taxation in both Canada and the United States, which could have a material adverse effect on our financial condition and results of operations. It is unlikely that we will pay any dividends on our common shares in the foreseeable future. However, dividends received by shareholders who are residents of Canada for purposes of the Income Tax Act (Canada) (the “Canadian Tax Act”) will generally be subject to a 30 percent U.S. withholding tax. Any such dividends may not qualify for a reduced rate of withholding tax under the U.S.-Canada income tax treaty (“U.S.-Canada Treaty”). In addition, a Canadian foreign tax credit may not be available under the Canadian Tax Act in respect of such taxes. Dividends received by shareholders resident in the United States will not be subject to U.S. withholding tax but will be subject to Canadian withholding tax under the Canadian Tax Act. In the event we pay any dividends, they will be characterized as U.S. source income for purposes of the foreign tax credit rules under the U.S. Tax Code. Accordingly, shareholders resident in the United States generally will not be able to claim a credit for any Canadian tax withheld unless, depending on the circumstances, such shareholders have an excess foreign tax credit limitation due to other foreign source income that is subject to a low or zero rate of foreign tax. Dividends received by shareholders that are residents of neither Canada nor the United States generally will be subject to U.S. withholding tax and Canadian withholding tax. These dividends may not qualify for a reduced rate of U.S. withholding tax under any income tax treaty otherwise applicable to our shareholders, subject to examination of the relevant treaty. Since we are classified as a U.S. domestic corporation for U.S. federal income tax purposes under section 7874(b) of the U.S. Tax Code, our common shares will be treated as shares of a U.S. domestic corporation and shareholders will be subject to the relevant provisions of the U.S. Tax Code and/or the U.S. Treaty.

Each shareholder should seek tax advice, based on such shareholder’s particular facts and circumstances, from an independent tax advisor, including, without limitation, in connection with our classification as a U.S. domestic corporation for U.S. federal income tax purposes under section 7874(b) of the U.S. Tax Code, the application of the U.S. Tax Code, the application of the U.S.-Canada Treaty, the application of U.S. federal estate and gift taxes, the application of U.S. federal tax withholding requirements, the application of U.S. estimated tax payment requirements and the application of U.S. tax return filing requirements.

We may incur significant tax liabilities under section 280E of the U.S. Tax Code.