Canadian Shareholder Class Action Lawsuit

On July 23, 2020, Blue Sky Realty Corporation filed a putative class action against the Company and its former Chief Executive Officer and former Chief Financial Officer in the Ontario Superior Court of Justice in Toronto, Ontario. On September 27, 2021, the court granted leave for the plaintiff to amend its claim (“Amended Claim”). In the Amended Claim, the plaintiff seeks to certify the proposed class action on behalf of two classes. “Class A” consists of all persons, other than any executive level employee of the Company and their immediate families (“Excluded Persons”), who acquired the Company’s common shares in the secondary market on or after April 12, 2019, and who held some or all of those securities until after the close of trading on April 5, 2020. “Class B” consists of all persons, other than Excluded Persons, who acquired the Company’s common shares prior to April 12, 2019, and who held some or all of those securities until after the close of trading on April 5, 2020. Among other things, the plaintiff alleges statutory and common law misrepresentation, and seeks an unspecified amount of damages together with interest and costs. The plaintiff also alleges common law oppression for releasing certain statements allegedly containing misrepresentations inducing Class B members to hold the Company’s securities beyond April 5, 2020. No certification motion has been scheduled. The Amended Claim also changed the named plaintiff from Blue Sky Realty Corporation to Timothy Kwong. The hearing date for the motion for leave to proceed with a secondary market claim under the Securities Act (Ontario) has been vacated. On March 3, 2023, the Company made a settlement offer to the plaintiff to fully resolve the Amended Claim. The plaintiff has not yet responded to the settlement offer.

Canadian Hi-Med Matter

On June 29, 2020, Hi-Med filed a notice of claim in the Supreme Court of British Columbia against the Company, the Company’s former Chief Executive Officers and other defendants, alleging that the defendants made materially false and misleading statements regarding certain proceeds from the issuance of long-term debt that were held in escrow to make interest payments in the event of a default thereof constituting oppression and seeking remedies including, but not limited to, repayment of Hi-Med’s Unsecured Debenture and damages of an unspecified amount.

Walmer Matter

On May 29, 2019, Walmer Capital Limited (“Walmer”) and Island Investments Holdings Limited (“Island”) filed a statement of claim in the Ontario Superior Court of Justice against MPX. The claim arose from the debentures (the “MPX Debentures”) issued by MPX Bioceutical Corporation (“MPX Corporation”) in May 2018, the majority of which debentures were redeemed on April 24, 2019 by MPX, a wholly-owned subsidiary of the Company and the successor entity to MPX Corporation following the MPX Acquisition. MPX withheld the redemption of approximately $1,250,000 of the original subscription amount of the MPX Debentures as MPX was unable to confirm valid payment of such debentures (the “Disputed Debentures”). The plaintiffs’ statement of claim alleged that the plaintiffs were entitled to the Disputed Debentures and sought immediate conversion of such debentures into the Company’s common shares. In addition, the plaintiffs sought damages including, but not limited to, for breach of the Disputed Debentures and related indenture in the amount of $111,000,000 and breach of a security subordination agreement in the amount of $3,500,000. On July 2, 2019, Walmer, Island, Walmer’s principal, Alastair Crawford (“Crawford”), Broughton Limited (“Broughton”) and Puddles 8 Limited (“Puddles”) filed a petition in British Columbia against the Company and its then directors based on the same facts as alleged in the statement of claim filed by Walmer and Island in the Ontario Superior Court of Justice and seeking a declaration that the respondents engaged in oppressive or unfairly prejudicial conduct and resulting damages. In September 2019, the parties to the Ontario action and the British Columbia petition agreed to consolidate the two proceedings into one action that addresses all issues in the British Columbia petition and agreed to discontinue the separate proceedings. On August 23, 2019, Walmer, Island, Crawford, Broughton and Puddles filed a notice of civil claim in the Supreme Court of British Columbia against MPX, the Company and its then directors consolidating the allegations made in the previously commenced Ontario action and British Columbia petition and seeking, among other things: (i) a mandatory order compelling MPX and the Company to convert the Disputed Debentures into common shares of the Company; (ii) damages for breach of the Disputed Debentures (and indentures) and breach of fiduciary obligations in the amount of $111,000,000; (iii) damages for breach of a security subordination agreement in the amount of $3,500,000; (iv) damages for breach of a consultancy agreement in the amount of $440,000 plus $150,000 plus certain warrants; and (v) damages for breach of the duty of good faith in the amount of $1,000,000. On October 31, 2019, the Company and MPX served the plaintiffs with a response and counterclaim. On December 3, 2019, the plaintiffs served (i) a notice of application seeking an order to strike the Company’s and MPX’s counterclaim against Timothy Childs, Island’s principal, in his personal capacity, on the basis that it alleges no cause of action against him and (ii) a notice of application for summary judgment. On February 11, 2020, the Company’s directors filed a defense to the plaintiffs’ claim with the Supreme Court of British Columbia.

Claim by Former Consultant

On August 19, 2021, Arvin Saloum (“Saloum”), a former consultant of the Company, filed a Demand for Arbitration with the American Arbitration Association (the “Arbitration Action”) against THCWC and iA AZ claiming a breach of a Consulting and Joint Venture Agreement (the “JV Agreement”) for unpaid consulting fees allegedly owed to Saloum under the JV Agreement. Saloum is claiming damages between $1,000,000 and $10,000,000. On September 7, 2021, THCWC and iA AZ filed Objections and Answering Statement to Saloum’s Demand for Arbitration. On November 18, 2021, THCWC and iA AZ filed a Complaint for Declaratory Judgment (“Declaratory Judgment Complaint”) with the Arizona Superior Court, Maricopa County (“Arizona Superior Court”), seeking declarations that: (i) the JV Agreement is void, against public policy and terminable at will; (ii) the JV Agreement is unenforceable and not binding; and (iii) the JV Agreement only applies to sales under the Arizona Medical Marijuana Act. On January 21, 2022, Saloum filed an Answer with Counterclaims in response to the Declaratory Judgment Complaint. The Declaratory Judgment Complaint remains pending before the Arizona Superior Court. The Arbitration Action is stayed, pending resolution of the Declaratory Judgment Complaint. The parties are currently engaging in discovery. The parties have agreed to participate in mediation to try and resolve the dispute, which is expected to occur in April or May of 2023.

Claim by Maryland License Holder

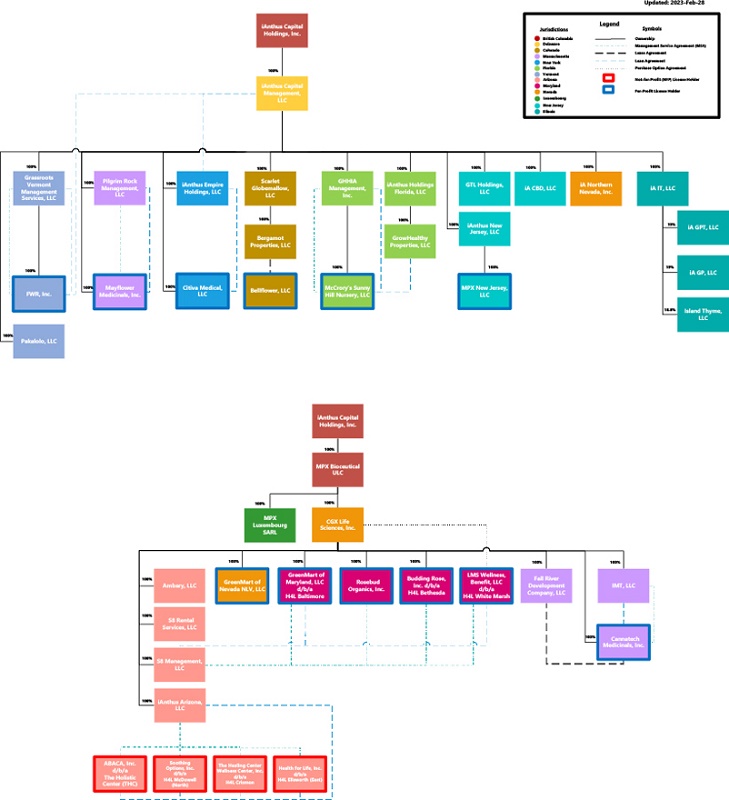

On May 23, 2022, CGX Life Sciences, Inc. (“CGX”), a wholly-owned subsidiary of the Company, filed a demand for arbitration (the “CGX Arbitration”) with the American Arbitration Association (“AAA”) against LMS Wellness Benefit LLC (“LMS”) and its 100% owner, William Huber (“Huber” and together with LMS, the “Defendants”) for various breaches under the option agreements entered into between CGX and LMS, on the one hand, and CGX and Huber on the other (collectively, the “Option Agreements”). Specifically, CGX is seeking: (i) an order finding the Defendants in breach of the Option Agreements and directing specific performance by the Defendants of their obligations under the Option Agreements to complete the sale and transfer of LMS to CGX; (ii) an order either tolling or extending the closing date under the Option Agreements; (ii) an order requiring Huber to restore LMS’ bank account of all sums withdrawn for the payment of contracts entered into in breach of the Option Agreements; and (iii) an order prohibiting Huber from withdrawing any further funds from LMS’ bank account. On June 8, 2022, the Defendants filed an Answering Statement, denying the allegations raised by CGX and sent a notice to CGX, purporting to terminate the Option Agreements.

In addition, on June 8, 2022, LMS filed a demand for arbitration (the “S8 Arbitration”) with the AAA against S8 Management, LLC (“S8”), alleging that S8 breached the Amended and Restated Management Services Agreement (the “MSA”) entered into between LMS and S8 on March 12, 2018. On June 24, 2022, the Defendants filed Motion to Consolidate the CGX Arbitration and S8 Arbitration. On July 5, 2022, CGX filed an opposition to the Defendants’ Motion to Consolidate and a cross-Motion to Stay the S8 Arbitration to allow the CGX Arbitration to proceed first. On July 26, 2022, the parties attended a preliminary conference with the arbitrator, at which conference the arbitrator preliminarily granted the Defendants’ Motion to Consolidate and denied CGX’s cross-Motion to Stay the S8 Arbitration. On October 7, 2022, CGX filed a dispositive motion for specific performance of Defendants’ obligations to complete the sale of LMS to CGX (claims (i) and (ii), above), which Defendants opposed. On October 31, 2022, the arbitrator granted CGX’s dispositive motion and ordered Defendants to complete the sale of LMS to CGX. The remaining claims asserted in the CGX Arbitration (claims (iii) and (iv), above) and the S8 Arbitration remain pending. On November 30, 2022, the Defendants filed a Petition to Vacate Arbitration Award and CGX filed its opposition on January 30, 2023. On February 3, 2023, the Defendants requested a hearing on the Petition to Vacate Arbitration Award. Both the Petition to Vacate Arbitration Award and request for a hearing remain pending before the Circuit Court for Baltimore County. CGX continues to prosecute its other two claims concerning Defendants’ use of LMS’ funds, and S8 continues to deny and defend against LMS’ contentions that S8 breached the MSA.

Annual General Meeting Petition

On June 20, 2022, Michael Weisser (“Weisser”) commenced a petition (the “Petition”) in the Supreme Court of British Columbia (the “Court”) against the Company and the Company’s former board of directors. In the Petition, Weisser sought: (i) a declaration that the affairs of Company and its then-board of directors were being conducted or have been conducted in a manner that is oppressive and/or prejudicial to Weisser; (ii) an order that Weisser is entitled to call and hold the Company’s annual general meeting for 2020 ( “2020 AGM”) on or before June 30, 2022 or a date set by the Court as soon as reasonably possible; (iii) alternatively, an order that the Company hold the 2020 AGM on or before June 30, 2022 or a date set by the Court as soon as reasonably possible; (iv) an order that the Company set the record date for the 2020 AGM; (v) an order that Weisser is entitled to appoint a chair for the 2020 AGM, or that the Court appoint an independent chair for the 2020 AGM; and (vi) an order that the Company be required to provide Weisser with an opportunity to review all votes and proxies submitted in respect of the 2020 AGM, no later than 24 hours in advance of the 2020 AGM. On June 22, 2022, Weisser was granted a short leave by the Court, which permitted a return date for the Petition of June 28, 2022. On June 24 2022, the Company closed the Recapitalization Transaction and the Company noticed the 2020 AGM, the annual general meeting for 2021 (“2021 AGM”) and the annual general meeting for 2022 (the “2022 AGM” and together with the 2020 AGM and 2021 AGM, the “AGMs”). As a result, Weisser’s Petition was rendered moot.

On November 14, 2022, Weisser filed an application (the “Application”) in the Petition proceeding, seeking to add the Secured Lenders and Consenting Unsecured Lenders as respondents to the Petition and to amend the Petition. Specifically, Weisser is seeking to amend the Petition to request: (i) a declaration that the affairs of the Secured Lenders, Consenting Unsecured Lenders, the Company and the powers of its then-directors have been and are continuing to be conducted in a manner that is oppressive and/or prejudicial to Weisser; (ii) an order setting aside and/or unwinding the closing of the Recapitalization Transaction; (iii) an order setting aside the results of the AGMs held on August 11, 2022; (iv) an order that the 2020 AGM be held by December 31, 2022; (v) an order that the Company set the record date for the 2020 AGM to hold the meeting by December 31, 2022; (vi) an order that for purposes of voting at the 2020 AGM, the shareholdings of the Company be those shareholdings that existed prior to the closing of the Recapitalization Transaction; (vii) an order that Weisser is entitled to appoint a chair for the 2020 AGM, or that the Court appoint an independent chair for the 2020 AGM; (viii) an order that the Company be required to provide Weisser with an opportunity to review all votes and proxies submitted in respect of the 2020 AGM, no later than 24 hours in advance of the 2020 AGM; and (ix) an order that pending the 2020 AGM, the Company’s current board of directors be replaced by an interim slate of directors to be nominated by Weisser. The Company intends to file a response to the Application, seeking that the Petition be dismissed as a collateral attack on the order of Justice Gomery dated October 5, 2020, approving the Recapitalization Transaction, and declaring as binding all of the releases set forth in Article 5 of the Plan of Arrangement.

Appeal of Florida Regulatory Approval of the Recapitalization Transaction

On October 29, 2021, the Florida Department of Health, Office of Medical Marijuana Use (the “OMMU”) approved the requested (the “Variance Request”) change of ownership and control of McCrory’s resulting from the closing of the Recapitalization Transaction. On November 19, 2021, Weisser filed a petition (as amended, the “Florida Petition”) with the OMMU, challenging the OMMU’s approval of the Variance Request. On February 3, 2022, the Florida Division of Administrative Hearings (“DOAH”) issued a Recommended Order of Dismissal, recommending that the OMMU enter a final order dismissing the Florida Petition for lack of standing. On May 4, 2022, the OMMU issued a final agency order (the “Final Order”), which accepted the recommendation of the DOAH and dismissed the Florida Petition for lack of standing. Weisser appealed the Final Order with the District Court of Appeal in the First District of Florida and filed his initial brief on November 9, 2022, which seeks a reversal of the Final Order. On February 3, 2023, the Company filed a Motion to Dismiss the appeal, which remains pending before the court.

46